Point‑of‑Care Coagulation Testing Devices Market: Empowering Rapid Hemostasis Decisions

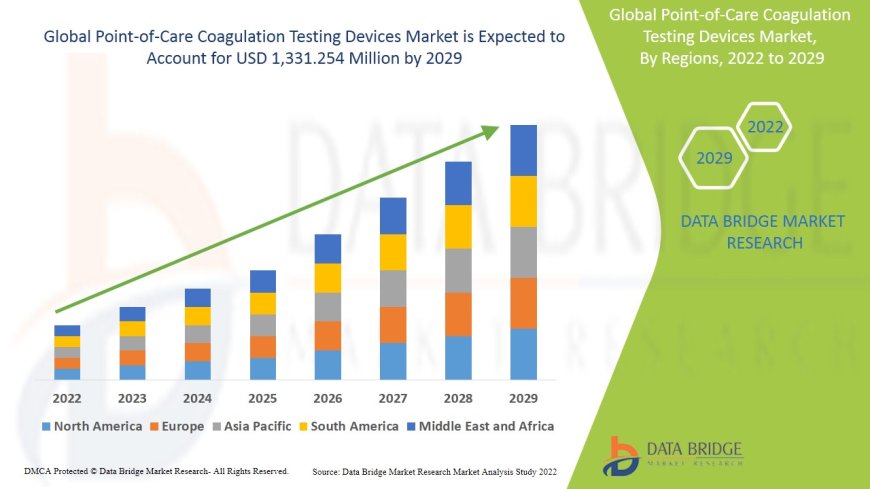

Data Bridge Market Research analyses that the point-of-care coagulation testing devices market is growing at a CAGR of 5.21% in the forecast period of 2022-2029 and is likely to reach USD 1,331.254 million in 2029.

Point-of-care (POC) coagulation testing devices deliver rapid, bedside assessments of hemostatic function by measuring blood clotting parameters such as INR, PT, aPTT, platelet function, D-dimer, fibrinogen and viscoelastic tests. They reduce delays associated with lab-based assays, guide anticoagulant therapy, monitor bleeding risk, and improve care in clinics, emergency settings, ORs, dialysis units, ICUs, and periprocedural contexts. Devices serve patients on warfarin, DOACs, with bleeding disorders, cardiac surgery candidates, trauma patients, and pregnancy-related thrombosis. Market growth is influenced by increasing anticoagulant use, aging population, surgical volumes, demand for personalized hemostasis management, and adoption of decentralized testing models.

The Evolution

Early coagulation tests in the 1930s were entirely lab-based and took hours. In the 1960s, semi-automated coagulometers emerged. The 1980s introduced viscoelastic techniques like TEG and ROTEM in surgical and trauma settings. The 1990s brought handheld PT/INR meters like CoaguChek enabling home monitoring for warfarin patients. Mid-2000s, cartridge-based devices suited for dialysis and perioperative settings became available. 2010s saw qLogic, ID NOW, and other POC platelet & coagulation function testers. 2020s have ushered in smartphone-interfaced devices, integrated AI algorithms, microfluidic POC profiling, and home-use apps for DOAC compliance. The COVID?19 pandemic shifted demand toward rapid D-dimer testing to assess coagulopathy. Recent devices offer multiplex panels analyzing multiple parameters in minutes with small blood volumes. The latest devices combine POC immunoassay modules with coagulation testing capabilities.

Market Trends

Demand for integrated systems capable of simultaneously delivering PT/INR, aPTT, fibrinogen, platelets, and viscoelastic measurements has grown. Adoption of DOACs is expanding the need for reversal agent monitoring capability at bedside. Smart devices with wireless data transmission, cloud analytics, and EMR integration are becoming standard. There is steady uptake of viscoelastic POC tests in trauma centers and ORs due to evidence linking use to reduced transfusions and better outcomes. Smaller sample volumes (~10 L) reduce patient blood losses. Mobile testing units are used in pre-hospital & rural settings. Artificial intelligence and predictive hemostasis software are guiding transfusion algorithms. Regulatory approvals for new D-dimer POC assays streamline ED usage. Subscription-based business models bundle devices with cartridge sales and data management platforms. Rising usage in veterinary medicine expands market scope. Geographically, North America leads followed by Europe and an emerging Asia-Pacific region. Portable coagulometers for home warfarin monitoring retain steady growth but growth is modest due to DOAC uptake.

Challenges

Analytical accuracy and alignment with central labs present challenges, especially with multi-parameter testing requiring frequent calibration. Cartridge and strip costs limit rehabilitation adoption, especially in low-resource settings. Training is needed to avoid misinterpretation of results and ensure correct usage and sample collection. Intra-device variability and environmental sensitivity, including temperature and humidity, may affect accuracy. Most devices still rely on capillary blood and fingerstick sampling, which can affect reliability. Regulatory approval differs across regions, complicating global deployment. Reimbursement frameworks are inconsistentPOC testing often reimbursed at lower rates than lab testing. Interferences from hemolysis, heparin presence, or low platelet counts may distort results. Integration into hospital IT systems and clinical workflows must avoid fragmentation. Younger devices need larger multicenter outcome trials to validate clinical utility. Covid-era supply chain challenges impacted consumable availability. Skepticism persists among traditional practitioners. Regulatory guidance around DOAC reversal monitoring is still evolving.

Market Scope

By Technology: PT/INR meters, PT/aPTT, viscoelastic devices (TEG/ROTEM), platelet function analyzers, D-dimer POC tests, multiplex microfluidics.

By Setting: Hospitals (OR/ICU/ED/Trauma), dialysis, clinics, pharmacies, EMS, home monitoring, veterinary.

By Application: Anticoagulant therapy management, bleeding disorder screening, perioperative transfusion guidance, trauma hemorrhage control, dialysis hemostasis, pre-administration of thrombolytics, pregnancy/peripartum assessment, outpatient management, veterinary.

Geographic Regions: North America (~40% share), Europe (~30%), Asia-Pacific (~20%), Latin America & MEA (~10%). Growth accelerated in APAC due to regulatory modernization, telehealth uptake, and rising chronic disease burden.

End-Users: Hospitals, clinical labs, dialysis units, warfarin clinics, EMS, ambulatory surgical centers, veterinarians, elderly care homes.

Key Players: Roche Diagnostics, Siemens Healthineers, Abbott Point of Care, Instrumentation Laboratory (Werfen), Danaher (Beckman Coulter), Hemosonics, Medical Depot, iCoagulation, Sinocare, Helena Laboratories, Roche CoaguChek, Quidel Ortho Clinical.

Market Size and Factors Driving Growth

The global POC coagulation testing device market was valued between USD?3.0?billion and USD?3.3?billion in 2023. Forecasts estimate growth to USD?5.15.5?billion by 2032, exhibiting a compound annual growth rate (CAGR) of 5.56.2%. For viscoelastic devices alone, market estimated at USD?800?million in 2023 and projected to exceed USD?1.5?billion by 2030 at ~8% CAGR.

Key growth factors

-

Increase in chronic cardiovascular diseases and atrial fibrillation driving anticoagulant prescriptions.

-

Perioperative and trauma surgeries rising, including orthopedic, vascular, and transplant interventions.

-

Pandemic-induced emphasis on rapid bedside diagnostics including D-dimer testing.

-

Adoption of DOACs expanding need for POC reversal monitoring instruments.

-

Healthcare decentralization through home-based monitoring.

-

Improved training frameworks allowing anticoagulation nurses & pharmacists to utilize POC devices.

-

Reimbursement alignment favoring POC testing in emerging markets under universal health schemes.

-

Microfluidic POC panels advancing small-sample protocols.

-

Telehealth integration enabling data flow and provider oversight.

-

Cloud-based analytics enabling hemostasis protocol optimization.

-

Cross-industry adoption in veterinary and military/field medicine sectors.

Conclusion

Point-of-care coagulation testing devices hold a central role in modern medicine, enabling precise, bedside hemostasis management in a variety of settings. A market worth over USD?3?billion is growing at 56% annually, with expansion driven by surgical volumes, anticoagulant usage, home monitoring trends, viscoelastic innovation, and telehealth integration. Innovation in microfluidic panels, AI-assisted interpretation, expanded reimbursement, and global expansion will accelerate adoption. Solutions addressing accuracy variability, cost reduction, workflow integration, and regulatory clarity will enable wider deployment. Market success lies in human-center design, training, cost-effective models, and outcome evidence proving improved patient care. POC coagulation technologies will remain essential in personalized, data-driven hemostasis care across global healthcare systems.

Tags

POC Coagulation Testing, Point-of-Care, PT/INR, aPTT, Viscoelastic Testing, TEG, ROTEM, Anticoagulant Monitoring, D-dimer, Hemostasis, Emergency Medicine, Perioperative Care, Telehealth Diagnostics, Microfluidic Assays, Home Monitoring, Veterinary POC, AI in Diagnostics, Personalized Medicine